What the heck is happening with startup valuations?

Looking at the past 4 years of public company data

If you’re interested in a weekly digest of these metrics, submit your email here.

TL;DR: All tracked sectors except Healthcare have on average regressed below pre-Covid levels. EdTech is faring by far the worst.

What are we tracking?

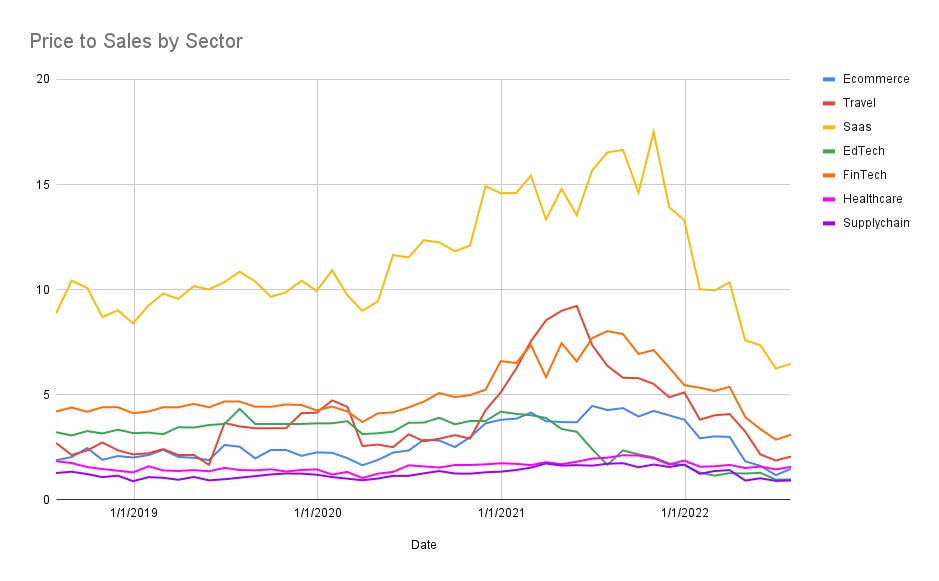

Startup valuations are largely tied to public company comps. As a company gets closer to IPOs, their valuations will follow more closely to their public counterparts. We track companies’ Price to Sales ratio, which is their forward looking revenue versus their public market cap. The graph above tracks the Price to Sales ratio of 7 sectors over the past 4 years.

From July 30th 2018 to July 30th 2022, price to sales ratio has adjusted accordingly:

Ecommerce: -21.4%

Travel: -23.8%

SaaS: -27.0%

EdTech: -69.6%

FinTech: -26.3%

Healthcare: +14.9%

Supplychain: -27.9%

What does this mean?

On one hand, if one were to just look at the past 2 years, it would seem like SaaS and FinTech have taken a gigantic hit, but on the macro, we’re only about 20% - 30% down from where things were 4 years ago. Zooming out really goes to show how rapidly and extremely some of these valuations were inflating over 2021 and 2022.

How has this affected startup valuations?

It’s hard to overlook how much private Fintech companies have gotten slapped in the past year. Private companies that have raised at previously large valuations in this space now have seen their valuations drop as investors are more hawkish on unit economics and revenue. Big potential movers are Plaid who raised at a previous $13B valuation but may not have the revenue to boot. Brex is in a similar position having raised at a $12B valuation. Klarna’s valuation has plunged -85% largely due to the company be comped to Affirm which is down also -85% from all time highs.

On the SaaS side of things, even though public comps have come down quite dramatically, SaaS companies with strong revenue numbers like Lattice will be able to grow into their $3B valuation. Likewise, Rippling, who also raised at a large $11B valuation has strong year over year revenue numbers and may grow into their hyped up valuations within a year or two.

Appendix

Which public companies are we tracking?

Ecommerce:

Amazon (AMZN), Alibaba (BABA), Ebay (EBAY), Etsy (ESTY), Figs Inc (FIGS), Chewy Inc (CHWY), Shutterstock (SSTK), Overstock (OSTK), Wayfair (W), Wish (WISH and 15 others.

Travel:

Booking (BKNG), Expedia (EXPE), Airbnb (ABNB), Trip Advisor (TRIP), Uber (UBER), Lyft (LYFT), Make My Trip (MMYT), Sabre (SABR), and 8 others.

Saas:

Oracle (ORCL), IBM (IBM), VMWare (VMW), Digital Ocean (DOCN), Cisco (CSCO), Akamai (AKAM), Confluent (CFLT), Atlassian (TEAM), Splunk (SPLK), Adobe (ADBE), Twilio (TWLO), Wix (WIX), SAP (SAP), Snowflake (SNOW), Couchbase (BASE), and 20 others

Edtech:

New Oriental (EDU), Bright Horizons (BFAM), Wiley Johnson (WLY), Coursera (COUR), Stride (LRN), Udemy (UDMY), Scholastic Corp (SCHL), Brightcove (BCOV) and 10 others

Fintech:

Block (SQ), Inuit (INTU), Paypal (PYPL), Global Payments (GPN), Bill.com (BILL), Coinbase (COIN), Sofi (SOFI), Toast (TOST), Upstart (UPST), Shift4 (FOUR), Payoneer (PAYO), Affirm (AFRM), and 14 others

Healthcare:

Accolade (ACCD), Signify Health (SGFY), OneMedical (ONEM), Hims and Hers (HIMS), 23andMe (ME), Clover Health (CLOV), Laboratory Corp (LH), Humana (HUM), Quest Diagnostics (DGX), and 20 others